Intelligently setting the Contractor's share ranges and share percentages

Introduction

At the April 2012 NEC User’s Group conference, the chair (Steve Rowsell) suggested that a good area for research would be on the setting of pain / gain share profiles under target cost contracts. I stuck up my hand and said that it had already been done by yours truly as part of my post-doctoral research between 1998 and 2000.

This article gives the conclusion of that research as an aid to practitioners when thinking about setting the share percentages and share ranges under the target cost options of the NEC3 family. This article assumes that the target cost option has been selected for the right reasons which, at a high level, are when:

- there is risk, whether threat or opportunity, with the target Prices which both parties can contribute to the management of. If only the Contractor that can significantly contribute, then a priced based option should probably be used; and / or

- there is a high likelihood of a significant volume of compensation events i.e. risk outside the target Prices, and the Employer wants transparency of cost in order to be able manage and assess them quickly. If the amount of change is expected to be very high, then the contract should probably be let as a cost reimbursable contract.

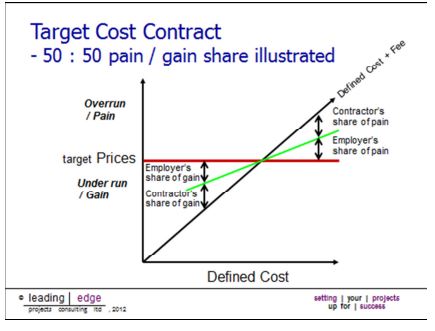

A diagram illustrating a 50 : 50 pain / gain share is given below.

In this diagram:

- the Defined Cost + Fee that the Contractor would be paid during the contract is the black diagonally rising line;

- the target Prices is the red horizontal line. During the contract this would only be adjusted due to compensation events; and

- the pain / gain line is the green line (in this diagram approximately a 50 : 50 share).

- to work out what the Employer would ultimately pay for any Defined Cost, you would go up from the horizontal axis of Defined Cost until you reach the green line and then go along horizontally.

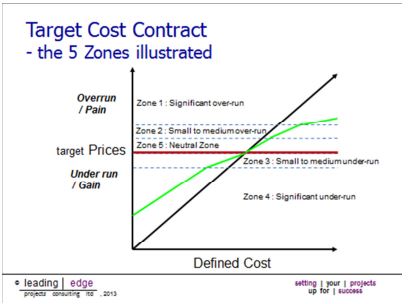

The 5-Zone Model

Having chosen a target cost contract for the right reasons, let us divide the share ranges into five zones. These are illustrated in the diagram below which has the same colour coding as the previous diagram.

Zone 1:

A significant over run of the target Prices which neither party could have reasonable predicted. In this Zone, the key question is who can best bear the over run and hence take the majority of the over run. For instance, a large employer, who has money coming in year on year will have much deeper pockets than a relatively small contractor making relatively small profit on what for them is a large contract. If too much risk is put on the Contractor then, instead of collaborating to reduce cost, he may well fight and squeal to transfer costs to the Employer through compensation events and cut corners on other aspects of the job. In all likelihood, this would be to the detriment of the Employer’s other objectives, such as quality, public relations etc.. Ultimately, they may become insolvent in which case all the risk will revert back to the Employer. Note that the Employer does not have to take all of the over-run and may wish to keep some motivation on the Contractor to perform by setting the Contractor’s share percentage at say 20%.

At the other end of the scale, you may have a relatively large Contractor (for whom the contract is a small one) and a relatively small Employer (for whom the contract is a large one). Here, the situation is reversed and it may be advisable to cap the overrun i.e. set it at 100% to the Contractor.

Zone 2:

A small to medium over run which is within the contemplation of the parties. Given that risk within the target Prices is generally within the Contractor’s predominant (but not necessarily exclusive) influence, it suggests that generally the Contractor should take the lion shares of any small to medium over-run e.g. 50%+. The less this is the case, the more the initial pain share should err towards a cost reimbursable contract with the Employer taking a greater percentage of over-run.

As an example of Zones 1 and 2, on the Channel Tunnel Rail Link the Employer had deleted the physical conditions compensation event on large civils contracts, but instead took 75% of any over-run up to 120% (Zone 2) of the target Prices and 90% thereafter (Zone 1). I.e. the contractors’ shares were 25% and 10%.

Zone 3:

A small to medium under run which is within the contemplation of the parties. The mirror image of the Zone 2 is that generally the Contractor takes the lion share of any small to medium savings compared with the target Prices and which are within the contemplation of the parties. Again, the less it is the case that the risks are within the Contractor’s control, the more initial gain share should err towards a cost reimbursable contract with the Employer taking a greater percentage of the savings.

Zone 4:

Significant savings which are beyond the reasonable contemplation of both parties. This is a point which applies to all four of the above Zones : the share of any savings or over run for each party should ideally be big enough to motivate both Parties to carry on working together to minimise costs.

In one framework, the employer was consulting with the pre-qualified contractors on the draft contract terms, including the share profile, and it was to be an early contractor involvement process whereby the final target was negotiated. They were proposing that contractors took all of the share of any over-run, half of the first 5% of any saving and beyond that, all savings would go to the employers. As it was being tendered recently in times of austerity, the contractors were likely to tender low fee percentages / have low margins to ensure they got on the framework. Thinking through the consequences of this from a contractor’s perspective :

- They would seek to add in (from an employer’s perspective) excessive risk prior to agreeing the target to protect the

- They would have no motivation to seek legitimate savings beyond the 5%

- When business picks up in a couple of year’s time, the employer’s projects will become unattractive causing them either not to bid or to put the ‘C’ team on it having got a nice risk contingency in the target downside.

However, as with any zone, there is no point in the Employer paying any more than what is sufficient to motivate the Contractor to carry on striving for savings. My gut feel is that less than a 20% share of any savings in Zone 4 would not motivate a typical contractor to seek out more savings.

Zone 5:

A neutral zone around the target for when the parties cannot agree. This neutral zone has been used in negotiated or open book pricing arrangements when the parties could not quite close out the difference to agree the target. The ‘zone’ spans the difference in their estimates which could be over how much risk should be included in the target. In this zone, the Contractor’s share lies somewhere between zero percent and the negative value of his fee percentage.

Let us illustrate the latter by saying that the Contractor’s fee percentage is 10% and he thinks that the target should be one million and fifty thousand pounds, but the Employer thinks it should be one million pounds. The target Prices are set at one million with the Contractor’s share of the first five percent of the over-run set at the 10% fee percentage. Consequently, in this zone, any additional Contractor’s fee is recovered through the pain mechanism. As a result, the Contractor’s margin is not eroded until he is exceeding his own estimate of one million and fifty thousand. Equally, the Contractor makes no additional margin until they have beaten the Employer’s lower estimate of what the contract should cost i.e. one million. In fact, under this arrangement most contractors have some motivation to save costs in this zone in order to increase their profit on turnover which is how many are evaluated. This is not the case if the Contractor’s share is set at zero percent in this zone.

When does each Zone start and finish

- If we assume that Zone 5 is not used, which will normally be the case, then the interface between Zones 2 and 3 will be the target Prices.

- Research in America, on cost plus incentive fee arrangements as they are known there, found that where savings were made, the largest proportion were in the 0 to 5% range, then dipped and rose up to spike at 10%, before tailing away fast.

Where savings of more than 10% were made, the view was that the target was initially set too high. This fits with my personal consultancy experience and suggests that the Zone 3 and 4 interface should be somewhere between 5 and 10%, but it will depend on the risk included with the target and the potential for jointly managing the threat out and opportunity in.

- The interface between Zone 1 and 2 has to be looked at from potential contractor’s perspective in terms when will they start to incur enough pain to significantly affect

- the attractiveness of the contract at bid and hence the risk premium they put within the target and

- their behaviours during the contract.

- Both of these are dependent on the pain allocated to them in Zone 2 i.e. for the same project and participants, the higher the pain in Zone 2, the lower the value of the Zone 1 / 2 interface when the Contractor would be feeling the same pain. And this in turn might affect the share of pain allocated to the Contractor in Zone 1.

Conclusion

The development of any effective incentive arrangement – and target cost contracts are no different – is an iterative process and has to consider the perspective of the other party you are trying to incentivise. Otherwise they may well be incentivised to do things you do not want!

The limits on this model are that it does not consider the interaction between the target cost pain / gain share mechanism and other incentive mechanisms, such as time based damages. Nevertheless, feedback from my contract strategy seminars shows that this is a useful model for developing pain / gain share arrangements.

Further reading

A fuller explanation of this model, with more examples to illustrate it, can either be found in:

- Broome J C and Perry J G, How practitioners set share fractions in target cost contracts, International Journal of Project Management, Vol. 20, No. 1, January 2002, or

- Chapter 8 of Broome J C, Procurement Paths for Partnering : A Practical Guide, Thomas Telford Ltd, 2002. (also available as an E-book and on a per chapter basis at www.icevirtuallibrary.com).

Lastly, an article which covers uses of multiple incentive mechanisms under NEC3 to stimulate improved contractor performance in line with employer objectives was published in Issue 50, April 2010 of this Newsletter and titled ‘Incentivisation under NEC3’.